Domestic Asset Protection Using

Limited Liability Companies (LLCs)

If you are reading this page, the chances are high that you have a need for asset protection planning. If that is not the case, please click here to read a short summary as to why 99% of people who have wealth need asset protection.

Domestic asset protection comes in many flavors. You will get a different answer to your asset protection questions depending on who you talk with.

See if the following makes sense:

- If you ask insurance agents about asset protection (in many states), their answer is to put your money into life insurance and annuities.

- If you ask pension consultants about asset protection, their answer is to put as much money as possible in an ERISA qualified plan.

- If you ask the typical CPA/accountant or attorney about asset protection (as a general statement), they will tell you that they don’t really understand the question.

- If you ask our firm this question, you will be asked a number of important questions, which would be followed up by a client questionnaire; and then a detailed summary of your problems and solutions will be delivered (to have a detailed analysis of your asset protection plan or lack thereof, please contact our office).

Domestic asset protection is a very diverse topic that virtually no one educates on today.

As a general statement, domestic asset protection revolves around the use of limited liability companies (LLCs).

Why not a C- or S-Corporation?

Because of the remedy, a creditor can obtain when asking a judge to make a debtor pay off a judgment or settlement.

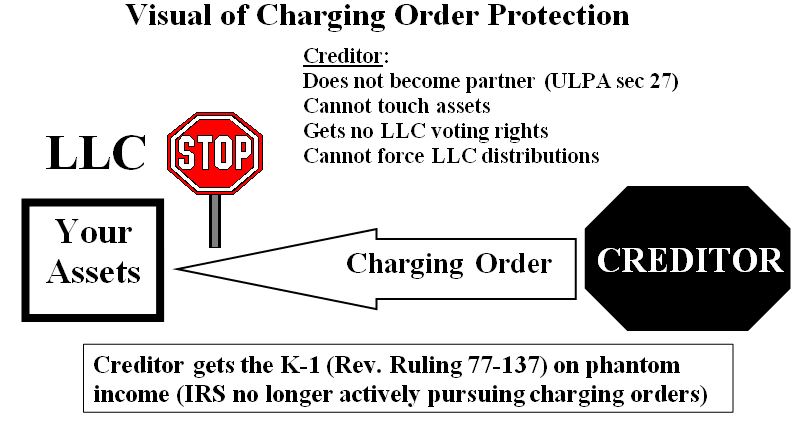

IF assets are owned by a properly set up LLC, a creditor who is asking the courts to have those assets turned over to the creditor can only obtain a “charging order” from the court (i.e., the court can’t invade the LLC and give those assets to the creditor).

What a creditor cannot get with a charging order

- A charging order does not transfer the interest in the LLC to the creditor or force the debtor to sell his/her interest and turn over the sale proceeds to the creditor.

- A creditor cannot force the LLC to sell assets.

- A creditor cannot force an LLC to distribute income.

What does a creditor get with a charging order?

The right to pay income taxes on income generated in the LLC but NOT distributed. There was a revenue ruling issued in 1977 (77-173) which states that a creditor who obtains a charging order can be treated as a partner for federal income tax purposes.

What if assets are owned by an individual or by a C- or S-Corporation?

The judge can direct the debtor (the loser of a lawsuit) to hand over assets in their own name directly to the creditor (i.e., no asset protection).

The following is an image that should help you visually understand how LLCs help protect assets.

Basically, a C- or S-Corporation is NOT a good tool when trying to protect personal assets such as:

Basically, a C- or S-Corporation is NOT a good tool when trying to protect personal assets such as:

— Family Home or Condominium

— Rental Property

— Non-Rental Property

— IRA

— Stocks or Mutual Funds

— Life Insurance

— Bank Account or CDs

— Planes, Boats, Automobiles, Wave Runners or Motorcycles

— Other business entity (especially S- or C-Corp stock)

— Any other collectible items that have value

If you have anything of wealth that you own in your own name (or that of your spouse or co-owned with your spouse), it is at risk from creditors.

Summary on Domestic Asset Protection

99%+ of the people with money in this country are not asset protected correctly. While the topics of domestic asset protection merits 50+ pages, the above is a quick little summary of the bread and butter asset protection tool (which is an LLC).

While an LLC is not a magic pill to be used as a cure-all, it is the foundation for any domestic asset protection plan and something that can start all clients on their way to protecting themselves from business creditors and personal creditors.

To get started down the road of asset protection, we recommend that you contact our office at ean@flintridgebenefit.com or {818} 790-8222 to set up an appointment.

What is Your Personal Risk Score?